| The Story of Silver | Source |

|

This is the story of silver’s transformation from soft money during the nineteenth century to hard asset today, and how manipulations of the white metal by American president Franklin D. Roosevelt during the 1930s and by the richest man in the world, Texas oil baron Nelson Bunker Hunt, during the 1970s altered the course of American and world history. FDR pumped up the price of silver to help jump start the U.S. economy during the Great Depression, but this move weakened China, which was then on the silver standard, and facilitated Japan’s rise to power before World War II. Bunker Hunt went on a silver-buying spree during the 1970s to protect himself against inflation and triggered a financial crisis that left him bankrupt.

Silver has been the preferred shelter against government defaults, political instability, and inflation for most people in the world because it is cheaper than gold. The white metal has been the place to hide when conventional investments sour, but it has also seduced sophisticated investors throughout the ages like a siren. This book explains how powerful figures, up to and including Warren Buffett, have come under silver’s thrall, and how its history guides economic and political decisions in the twenty-first century.

| Chapter 1 Chapter 2 Chapter 3 Chapter 4 Chapter 5 Chapter 6 Chapter 7 Chapter 8 Chapter 9 Chapter 10 Chapter 11 Chapter 12 Chapter 13 Chapter 14 Chapter 15 Chapter 16 Chapter 17 Chapter 18 Chapter 19 Chapter 20 Chapter 21 Chapter 22 Chapter 23 |

Introduction: Obsession Hamilton’s Design Solving the Crime of 1873 Free Silver Seeds of Roosevelt’s Manipulation FDR Promotes Silver Silver Subsidy China and America Collide Bombshell in Shanghai Silver Lining Costly Victory JFK’s Double Cross LBJ Nails the Coffin Shut Psychiatrist’s Meltdown Battle Lines Nelson Bunker Hunt Heavyweight Fight Saudi Connection Silver Soars Collapse The Trial Buffett’s Manipulation? Message from Omaha The Past Informs the Future Bibliography Endnotes |

xi 1 3 6 8 10 12 14 18 25 28 30 34 38 43 44 49 52 55 61 68 74 77 81 82 88 |

A lover of silver will never be satisfied with silver.

—Ecclesiastes 5

To

Danny

You left us too soon

I did not know Nelson Bunker Hunt, whose death in 2014 spawned this book project, but many who knew him well shared their insights and recollections. I could not have written the story of silver without them. Phil Geraci of the Kay Scholer law firm that represented the Hunt brothers during their silver manipulation trial was a young lawyer back then and provided key personal observations from his six-month interaction with the Hunts. His assistant Patricia Apuzzo made it easy to use the related material.

Henry Jarecki, whose business dealings with the Hunts while chairman of Mocatta Metals Corporation lasted more than a decade, gave me access to his unpublished manuscript that offered details unavailable elsewhere. His assistant Emily Goodnight made the process enjoyable and productive. Professor Jeffrey Williams served as an expert witness for the Hunts at their 1988 trial and provided copies of plaintiff and defendant expert reports that had been stored in his garage since then. I also relied on his excellent book on the economic testimony at the trial.

But this book is more than just about the Hunts. It is the story of silver, so at the beginning I spent a day with silversmith Geoffrey Blake at Old Newbury Crafters in Amesbury, Massachusetts, watching him mold the white metal into sterling silver flatware with the same tools and techniques that Paul Revere might have used.

The ancient craft practiced in Blake’s dusty basement workshop contrasted with the modern spectrograph used by Don and Angelo Palmieri in their Gem Certification & Assurance Lab to determine whether sterling silver jewelry contains the required 92.5% pure silver. But some things do not change. I watched Albert Robert (Irina and Gabriel’s cousin) of the New York Gold Refining Company turn a silver coin into molten metal by heating it in a blackened crucible over an open flame as in ancient times.

My research work benefited from the cheerful effort of many individuals. I owe Carol Arnold-Hamilton, Alicia Estes, and Robert Platt, librarians at NYU’s Bobst, for recovering source material that challenged Google’s algorithms. Jack Shim, an outstanding PhD student at NYU Stern, and Omer Morashti, a great Stern MBA, analyzed the data with surgical skill. Bob Oppenheimer shared firsthand observations of the silver ring at the Commodity Exchange (Comex). Bernard Septimus, my friend for as long as I can remember, applied his biblical expertise to keep my references consistent with modern scholarship. Seth Ditchik and Bruce Tuchman read an early draft and molded the framework of the story for the better. Dick Sylla, Ken Garbade, and Paul Wachtel read the entire manuscript as if it were their own and scrubbed the fuzzy logic from the final product. Peter Dougherty, my editor at Princeton University Press, offered sage advice and gentle encouragement throughout the process. His e-mails at 5 a.m. were just the tip of the iceberg. My wife, Lillian, let me work on the book whenever I wasn’t playing golf, read every word, and excised most (but certainly not all) of the annoying metaphors. And I apologize to my children and grandchildren for not calling the book “Silber on Silver,” a unanimous recommendation at our family gatherings that fell to the cutting room floor like so many other gems.

No one needs to read the notes appearing at the end of the book, but they are there to expand on historical details and to provide technical information. The notes contain citations to newspapers, periodicals, academic articles, and books to support specific opinions and quotations appearing in the text. Statistical tests and a precise explanation of silver price data also appear in the notes. Silver prices usually refer to the price of physical silver in the form of bullion bars. These are sometimes called cash prices to distinguish them from prices in the futures market that become important in the second half of the book. The silver price data come from a variety of sources:

- annual data during the nineteenth century come from the Annual Report of the Director of the Mint, Washington, DC: Government Printing Office, 1936;

- daily data on silver prices during the 1930s were hand-collected from the Wall Street Journal, which published cash market quotations by bullion dealer Handy & Harman;

- daily data on cash prices since 1947 and futures prices since 1963 were purchased from the Commodity Research Bureau (CRB), an independent data distributor that was a division of Knight-Ridder Financial Publishing and is now a division of Barchart.com, Inc., a Chicago-based vendor of financial data; and finally,

- daily data on the London silver fix since 1968 come from the London Bullion Market Association as published by Quandl, an internet provider of economic and financial data.

| Figure 1 Figure 2 Figure 3 Figure 4 Figure 5 Figure 6 Figure 7 Figure 8 Figure 9 Figure 10 Figure 11 Figure 12 Figure 13 Figure 14 Figure 15 Figure 16 Figure 17 Figure 18 Figure 19 Figure 20 Figure 21 |

National Photo Company Collection, Prints & Photographs Division, Library of Congress, LC-DIG-npcc-24200 Everett Historical / Shutterstock.com Brady-Handy Collection, Prints & Photographs Division, Library of Congress, LC-DIG-cwpbh-04797 Prints & Photographs Division, Library of Congress, LC-USZ62-22703 Prints & Photographs Division, Library of Congress, LC-USZ62-86702 Bettmann / Contributor / Getty Images nsf / Alamy Stock Photo Bettmann / Contributor / Getty Images National Numismatic Collection, National Museum of American History Sueddeutsche Zeitung Photo / Alamy Stock Photo National Numismatic Collection, National Museum of American History (top) Photograph by Dimitri Karetnikov; (bottom) United States Mint John Marmaras Photography AP Photo/Charles Wenzelberg Central Press / Stringer / Hulton Archive / Getty Images doomu / Shutterstock.com Bettmann / Contributor / Getty Images Bettmann / Contributor / Getty Images Classical Numismatic Group, Inc. www.cngcoins.com Bloomberg / Contributor / Getty Images United States Mint |

The outline of this book when I started five years ago differs considerably from the final product. History surprised me with events and personalities that changed my thoughts and perceptions. I have shared those stories with you throughout this book and hope they are as pleasurable, instructive, and exciting for you as they were for me.

|

William L. Silber is the Marcus Nadler Professor of Economics and Finance at the Stern School of Business, New York University. He received NYU’s Distinguished Teaching Medal in 1999 and was voted Professor of the Year by Stern MBA students in 1990, 1997, and 2018. He received his PhD in economics from Princeton University and has written about monetary economics and financial history, including seven books, most recently, Volcker: The Triumph of Persistence, which chronicles the career of former Federal Reserve Chairman Paul Volcker. The Volcker biography won the China Business News Financial Book of the Year in 2013, was a finalist in the Goldman Sachs / Financial Times Business Book of the Year in 2012, and was named “One of the Best Business Books of 2012” by Bloomberg Businessweek. His first book, Money, coauthored with Lawrence Ritter, made a serious topic fun to read.

William L. Siber at Wikipedia

By the Same Author

Volcker: The Triumph of Persistence

When Washington Shut Down Wall Street: The Great Financial Crisis of 1914 and the Origins of America’s Monetary Supremacy

Financial Options: From Theory to Practice (coauthor)

Principles of Money, Banking, and Financial Markets (coauthor)

Financial Innovation (editor)

Money (coauthor)

Portfolio Behavior of Financial Institutions

(IN CHRONOLOGICAL ORDER)

|

Alexander Hamilton |

|

|

John Sherman |

|

|

William Jennings Bryan |

|

|

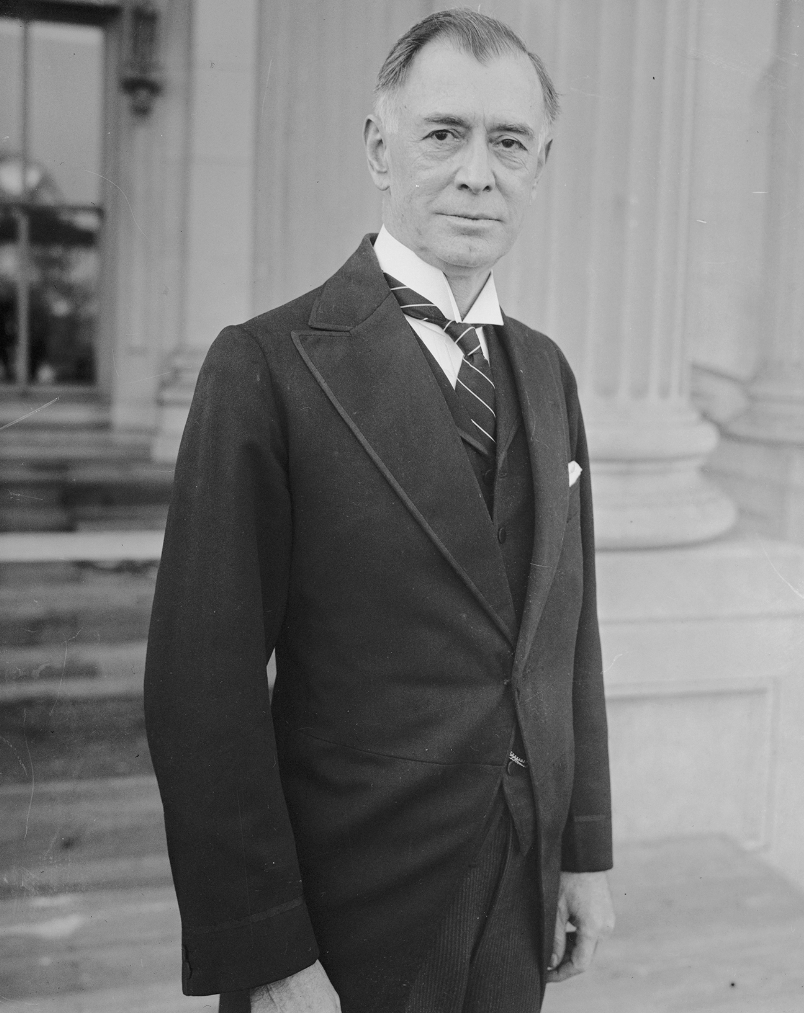

Key Pittman |

|

|

Franklin Delano Roosevelt |

|

|

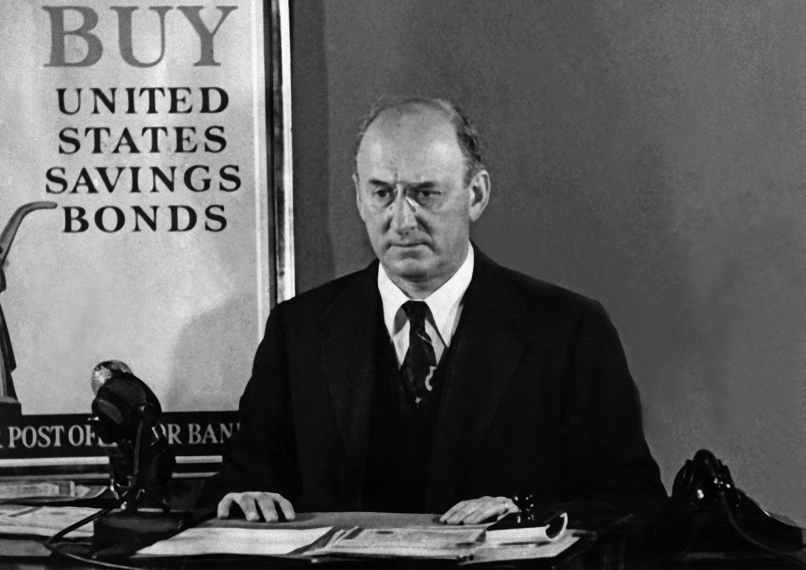

Henry Morgenthau |

|

|

John Fitzgerald Kennedy |

|

|

Lyndon Baines Johnson |

|

|

Henry Jarecki |

|

|

Nelson Bunker Hunt |

|

|

Warren Buffett |

|

Lamar Hunt, the thirty-four-year-old owner of the Kansas City Chiefs football team, negotiated the merger of the upstart American Football League with the older and well-established National Football League in 1966, creating the most successful sports enterprise in America. Hunt also invented the name Super Bowl, originally the championship game between the two leagues, and now the most popular single sporting event in the country. He explained the origin of his inspiration: “My daughter, Sharron, and my son, Lamar Jr., had a children’s toy called a Super Ball, and I probably interchanged the phonetics of ‘bowl’ and ‘ball.’”1

The first Super Bowl was played in January 1967 and pitted Hunt’s Kansas City Chiefs against Vince Lombardi’s Green Bay Packers. The Packers walloped the Chiefs 35–10 and were awarded the Super Bowl trophy, a seven-pound sterling silver football made by Tiffany & Company. Winners of the annual Super Bowl since then have received an identical creation, now called the Vince Lombardi Trophy, with the winning team’s name engraved on the pedestal by Tiffany craftsmen.

Lamar was proud of his franchise, especially after his Chiefs won the Super Bowl in January 1970, but he had no way of knowing that ten years later the trophy itself would be worth twenty-five times its original value, and not just for sentimental reasons. In January 1980 the price of silver had jumped to $50 an ounce, a modern record that still stands, and Lamar, together with his older brothers Nelson Bunker Hunt and Herbert Hunt, would be accused of rigging the price of the white metal in the boldest commodities market manipulation of the twentieth century.2

Lamar, Nelson Bunker, and Herbert were sons of H.L. Hunt, a poker-playing oil tycoon whose right-wing political outlook equated New York’s liberal Republican governor, Nelson Rockefeller, with Cuba’s Fidel Castro. The family patriarch taught his children to distrust government, especially its paper currency, and to invest in real things, such as oil, land, and precious metals. He established trusts for his children, including shares in the family’s billion-dollar crown jewel, the Placid Oil Company, which served as a funding source for their business ventures. The tall and trim Lamar, as mild mannered as an accountant, concentrated on football during the 1960s, while his outspoken older brother Bunker, as Nelson was called, concentrated on racehorses and oil fields. Bunker was a pear-shaped 250-pounder who enjoyed the limelight that came with being the family spokesman. A speculator like his father, Bunker may have been the richest man in the world after oil was discovered in Libya, where he owned the drilling rights. Bunker had made his deal with Libya’s King Idris, but before he could enjoy all the fruits of his speculations, insurgents led by Muammar Qaddafi overthrew the monarchy in 1969 and soon after nationalized the oil fields. Bunker was still a billionaire, when a billion dollars was real money, but the incident increased his distrust of government.

Bunker affirmed his conservative credentials by joining the John Birch Society, the Tea Party of its day, and began investing in silver because he feared government spending would produce inflation and erode the value of the U.S. dollar.3 He also thought he could store his cache of the precious metal on his two-thousand-acre Circle T ranch near Dallas without worrying about Qaddafi. But his speculation quickly turned into an obsession, and even Texas was not big enough for his holdings. Between 1973 and 1979 he led his brothers in accumulating almost 200 million ounces of the white metal, stored in New York, London, Switzerland, and other locations that may not have been publicly disclosed. The Hunt silver was worth about $2 billion in September 1979. Four months later, when silver hit $50 an ounce, it came to nearly $10 billion.

Then it all disappeared. Within a year Bunker Hunt was forced to pledge his shares in Placid Oil as collateral for a billion-dollar loan to avoid bankruptcy. He had personally borrowed heavily to buy silver and the value of his leveraged holdings collapsed when prices fell back to $10 an ounce, a drop that rivaled the decline in the Dow Jones stock index during the Great Depression. He and his brothers were then found liable for conspiring with Saudi Arabian sheikhs to corner the silver market during their speculative binge. Bunker Hunt declared personal bankruptcy after the trial and lost prized possessions to his creditors, including fifteen ancient Greek vases and a collection of silver coins dating from the Roman Empire.4 When an older sister asked what had happened, he answered, “I was just trying to make some money.”5

The Hunts were not the first nor the last to be seduced by the white metal. In 1997 Warren Buffett, perhaps the most successful investor of the past fifty years, bought more than 100 million ounces, almost as much as the Hunts, and drove the price of silver to a ten-year peak. In 1933 Franklin Delano Roosevelt raised the price for silver at the U.S. Treasury to mollify senators from western mining states while ignoring the help it gave Japan in subjugating China. And in 1918 Senator Key Pittman of Nevada subsidized his home state constituents by sponsoring legislation to sell silver to India during the Great War. But the white metal has been more than just a vehicle for personal advancement to Americans; it has been part of the country’s monetary system since the founding of the Republic and is woven into the fabric of history like the stars and stripes.

1. Lamar Hunt, a Force in Football, Dies at 74, New York Times, December 15, 2006, p. C12.

2. The related designation “boldest futures manipulation of the twentieth century” is from Burton Malkiel, A Random Walk Down Wall Street, rev. ed. (New York: Norton, 2015), p. 417. The peak price was an intraday high of $50.36 for spot silver (i.e., for the January futures contract) recorded on January 18, 1980, on New York's Commodity Exchange (see New York Times, January 19, 1980, p. 36). An intraday high of $50.50 was recorded on the Chicago Board of Trade.

3. For Bunker's association with the John Birch Society, see Stephen Fay, Beyond Greed (New York: Viking Press, 1982), pp. 18-19.

4. Bankrupt Hunt Brothers Bid Adieu to Art Collections Worth Billions, Chicago Tribune, May 10, 1990, p. C1.

5. Nelson Bunker Hunt, 88, Oil Tycoon with a Texas Size Presence, Dies, New York Times, October 22, 2014, p. A24.

Perhaps the most famous speech in American electoral politics, Nebraska Congressman William Jennings Bryan’s “Cross of Gold” sermon at the 1896 Democratic convention, was all about silver. Bryan became the party’s nominee for president after delivering an address that would make a modern televangelist blush: “I come to speak to you in defense of a cause as holy as the cause of liberty—the cause of humanity … that all believers in free coinage of silver in the Democratic Party should organize and take charge of and control the policy of the Democratic Party … We do not come as aggressors. Our war is not a war of conquest. We are fighting in the defense of our homes, our families, and posterity.”6 Bryan’s cause, the resurrection of silver as a monetary metal, aimed to rectify the injustice perpetrated by the Crime of 1873, which discontinued the coinage of silver dollars that Congress authorized in 1792 and established gold as king of American finance. The demonetization of silver sparked a great deflation in the United States during the last quarter of the nineteenth century, with declining agricultural prices provoking resentment among midwestern farmers against East Coast bankers. The Wonderful Wizard of Oz, which has entertained millions since it was published in 1900, is an allegory of the contemporary class warfare.

The abundance of silver in America during the 1870s made it the metal of the people, synonymous with cheap money compared with the more restrictive supply of currency under the gold standard. Bryan viewed remonetizing the white metal as a way to promote inflation to reduce the burden of mortgages owed by farmers to the banks. A century later, during the 1970s, the Hunts invested in silver as a bulwark against inflation, a rock-hard asset to protect their fortune against the spendthrift ways of the government. This is the story of silver’s transformation from soft money during the nineteenth century to hard asset today, and how manipulations of the white metal have altered the modern world; but to understand the attraction of silver to politicians and its vulnerability to speculators and schemers requires historical perspective.

Silver is the preferred protection against government defaults, political instability, and inflation for people in most countries, a place to hide when conventional investments sour. In the three years following the financial crisis of 2008, when banks teetered on the brink of insolvency and the government debts of Italy, Ireland, and Greece resembled junk bonds, anxious investors drove up the price of silver by almost 400%, an increase greater than ten years of Warren Buffet’s Berkshire Hathaway stock.7 But the precious metal is more than just another safe-haven investment. For centuries it has been hammered by silversmiths into serving platters, candlesticks, and wine goblets for the upper classes. Families display these heirlooms with pride in their dining room cupboards to highlight an affluent past, but during bad times they are quietly sold for cash.

Silver has also been the monetary standard of almost every country in the world, including China and Saudi Arabia in the twentieth century, Great Britain in the seventeenth, and Biblical Egypt. Britain dominated world commerce with the gold standard during the nineteenth century, but its currency is still called “the pound sterling,” a paradoxical reference to sterling silver as the standard. The word “sterling” means that a coin, candelabra, or Super Bowl trophy contains 92.5% pure silver, with the remaining 7.5% usually consisting of copper for strength. A mixture of nitric acid and potassium dichromate produces a different color on a sample scraping of “fine” silver, which is 99.9% pure, compared with sterling, and there is little to dispute once the sample has been assayed (tested) professionally.8 Governments guarantee the purity and weight of coins minted from precious metals to make the currency generally accepted without further testing, and silversmiths engrave 925 or the word sterling on their work to certify its quality. Queen Elizabeth I, daughter of Henry VIII and Anne Boleyn, ascended the throne in 1558 and two years later made the metal backing the British currency one pound of sterling silver.9 This so-called “ancient right standard of England” originated in the eleventh century under William the Conqueror, but had been debased by the gluttonous Henry before Elizabeth’s rescue.10 The sterling reference stuck despite Britain’s switch to gold and survives today even though the silver content of the pound is long gone.

The clash between ornamental demands by silversmiths and government coinage often had surprising consequences. Louis XIV, the absolute monarch of France for seventy years until his death in 1715, turned the magnificent silver furniture and tableware in the Palace of Versailles into bullion bars for minting by his Treasury.11 Silver dishes with matching place settings became common currency. The remaining French nobility had little choice but to follow the king’s example—Louis is famous for the proclamation, “L’État, c’est moi” (I am the state). The results were fiscal credibility in France and a scarcity value in the surviving silver antiques.

6. Speech Concluding the Debate on the Chicago Platform, in William Jennings Bryan, The First Battle: A Story of the Campaign of 1896 (Chicago: W.B. Conkey Company, 1896), pp. 199-200.

7. The cash price of silver on September 12, 2008, the Friday before the investment bank Lehman Brothers announced its bankruptcy, was $10.87 per ounce. Three years later on September 12, 2011, during the height of the European sovereign debt crisis, silver was $40.26 per ounce, for an increase of 370% over the three year period. Berkshire Hathaway closed at $103,800 on September 12, 2011, compared with a price of $68,000 on September 10, 2001, an increase of less than 100%. Note: As described in “From the Author” at the beginning of this book, cash prices after the 1930s come from the Commodity Research Bureau (CRB) database (the SIY series), unless noted otherwise. Berkshire Hathaway stock prices are from Yahoo! Finance.

8. I witnessed this test conducted by Donald and Angelo Palmieri of the Gem Certification & Assurance Lab (GCAL), 580 Fifth Avenue, New York City, although it was not easy for me to distinguish the colors. They also confirmed this test with a more modern X ray fluorescence technique. For a discussion of assaying by fire from ancient times to the present see J.S. Forbes, Hallmark: A History of the London Assay Office (London: Unicorn Press, 1999), pp. 20-24. Also see

http://www.sciencecompany.com/HowtoTestGoldSilverandOther PreciousMetals.aspx

9. See A.E. Feavearyear, The Pound Sterling: A History of English Money (Oxford: Clarendon Press, 1931), chap. 4; and Seymour Wyler, The Book of Old Silver (New York: Crown, 1937), p. 7. According to Thomas Sargent and Francois Velde, The Big Problem of Small Change (Princeton, N.J.: Princeton University Press, 2002), pp. 82-83, One pound represented different amounts of gold and silver at different times,” which may be true, but both Wyler and Feavearyear confirm that Elizabeth promulgated the sterling standard of “11 ounces, 2dwt.” There are 20 pennyweights (dwt) in a troy ounce so sterling meant 11.1 troy ounces, which is .925 of a troy pound (= 12 troy ounces).

10. Feavearyear, Pound Sterling, p. 8.

11. Daniëlle O. Kisluk-Grosheide and Jeffrey Munge, The Wrightsman Galleries for French Decorative Arts (New York: Metropolitan Museum of Art, 2010), p. 106.

Governments no longer coin silver as currency but rising industrial demands compete with silversmiths for the available supply of the white metal. Photographic film produced by the camera company Eastman Kodak usually consumed more silver in a year than the jewelry industry.12 Now that digital cameras have made photographic film obsolete (driving Kodak into bankruptcy in 2012), the electronics industry dominates commercial uses. Silver, called a noble metal, along with gold and platinum, because it resists corrosion, is the best conductor of electricity and is used in circuit breakers, switches, fuses, and other electrical components. Modern technology has also exploited silver’s antibacterial properties. In 2006 the giant Korean manufacturer Samsung introduced a washing machine that releases silver ions in the wash cycle to help sanitize the laundry.13 Specialty retailer Sharper Image advertised a plastic food container infused with silver nanoparticles to keep food fresher, which received positive feedback on Amazon from users.14 And in 2017 Colgate University in central New York state sprayed its locker rooms with a decontaminating fog of hydrogen peroxide and silver to combat the deadly MRSA staph infection.15 The white metal’s industrial demand now exceeds its combined use in jewelry, bullion bars, and commemorative coins.16

Silver attracts manipulators because occasional bursts of speculative fever clash with rising commercial use, especially when citizens fear political unrest. The resulting price gyrations allow conspirators to promote higher prices with relatively little effort while also camouflaging their manipulation. On November 4, 1979, during the height of the alleged Hunt conspiracy to corner the silver market, Iranian students invaded the U.S. embassy and took American citizens hostage.17 The ensuing political crisis contributed to the tripling of silver prices during the next three months, masking the footprints of the manipulators.18

Gold is the primary store of value for those who mistrust the government, but silver remains the refuge of choice for most people because it is cheaper and more accessible. A standard 100-ounce bar of silver, about the size of three Hershey bars stacked on top of each other, costs about $1,700 today compared with a price of $130,000 for a 100-ounce gold bar. The relatively small dollar size of the silver market makes the white metal more volatile than the yellow, where a million-dollar order from anxious buyers and sellers makes a bigger impact.19 Silver led the jump in precious metals after the 2008 financial crisis with nearly a 400% increase compared with almost 250% for gold.20

For most of recorded history paper currency was acceptable in everyday transactions because governments promised to exchange those pieces of paper for gold or silver, which gave money intrinsic value. U.S. citizens could exchange dollars for gold at the rate of $20.67 per ounce at the U.S. Treasury until 1933, and foreign governments could do the same at $35.00 per ounce between 1934 and 1971. President Nixon suspended the Treasury’s gold obligations on August 15, 1971, ending the last connection between the dollar and precious metals.

All countries now issue fiat currency, paper money backed only by the creditworthiness of the government. The verdict remains uncertain on this relatively new worldwide experiment in pure paper currency because governments have often abused their right to print money, destroying its value, as in the 1920s hyperinflation in Germany.21 Those concerned that the experiment will fail, such as the Hunts in the 1970s and the Tea Party today, seek refuge in the ageless storehouses of gold or silver. The great English economist David Ricardo, who learned a lot about money as a successful speculator, wrote almost two hundred years ago, “Experience, however, shows that neither a State nor a Bank ever have had the unrestricted power of issuing paper money, without abusing that power.”22 Ricardo recommended that “the issue of paper money ought to be under some check and control; and none seems so proper for that purpose as that of subjecting the issuers of paper money to the obligation of paying their notes, either in gold [or silver] coin or bullion.”23 Anchoring currencies to precious metals promoted price stability but caused controversy as well.

The United States, at the urging of Secretary of the Treasury Alexander Hamilton, established the silver dollar alongside gold in 1792 as America’s currency. The two metals vied for public attention under this bimetallic standard until Congress passed the Coinage Act of 1873, eliminating the official status of silver and making gold the sole backing of America’s money.24 The scarcity of the yellow metal caused widespread price deflation over the next twenty-five years, and the reduced government demand for silver contributed to its decline in value of more than 50%.25 The subsequent outcry in western mining states for Congress “to do something for silver” made headlines throughout the country.26 William Jennings Bryan rode a silver train of resentment to the 1896 Democratic nomination for the presidency that ended in his defeat by William McKinley. Bryan ran twice more for the White House and lost, but none of those setbacks muffled the agitation for silver, which continued well into the twentieth century.

During the Great Depression, after the price of silver hit a record low of 24¢ an ounce, Democratic Senator Key Pittman of Nevada, the powerful chairman of the Senate Foreign Relations Committee, urged President Roosevelt to restore the white metal’s full monetary status.27 In exchange, Pittman promised the support of fourteen senators from western mining states for Roosevelt’s controversial New Deal legislation. FDR responded with a series of purchase programs for silver, beginning with an executive order on December 21, 1933, directing the U.S. Treasury to buy the domestically produced metal at 64.5¢ an ounce, a premium of 50% above the free market price of 43¢.28 The subsidy and the doubling of silver prices during Roosevelt’s first administration gave “the silver miners and speculators much for which to be thankful,” according to contemporary financial observers.29 Senator Pittman agreed and described FDR’s benevolence as a “Christmas present.”30

Pittman made good on his promise. He delivered the “silver bloc” senators in support of FDR’s 1933 pump-priming legislation, helping to jump-start the domestic economy, but U.S. diplomacy suffered a major blow. The higher price paid by the Treasury attracted silver from the rest of the world, especially from China, whose currency was backed by the precious metal. Despite local laws restricting exports, speculators smuggled silver out of Shanghai to profit on world markets and ultimately forced China to abandon the silver standard when that country was most vulnerable.31 It was 1935 and China, led by American ally Chiang Kai-shek, faced an internal threat from Mao Tse-tung’s communist insurgents and an external threat from Imperial Japan. Roosevelt’s Treasury secretary, Henry Morgenthau, worried that China’s insecure government, weak economy, and susceptibility to Japanese aggression made her especially vulnerable to the dislocations arising from American silver policy.32

Morgenthau was right to worry. Roosevelt’s pro-silver program to please western senators helped the Japanese military subjugate a weakened China and boosted Japan’s march towards World War II, demonstrating the danger of formulating domestic policy without considering international consequences. Was FDR’s price manipulation less criminal than Nelson Bunker Hunt’s? Reading this book will let you make an informed judgment.

12. William E. Brooks, “Silver,” in U.S. Department of the Interior & U.S. Geological Survey. Minerals Yearbook 2008, vol. 1, Metals and Minerals (Washington, DC: Government Printing Office, 2010), p. 68.2, available at

https://babel.hathitrust.org/cgi/pt?d=msu.31293031621463;view=1up;seq=902

13. See Rhonda L. Rundle, “This War against Germs Has a Silver Lining,” Wall Street Journal, June 6, 2006, updated 12:01 a.m. “Now, silver is showing up as a bacteria- and odor-fighting material in a range of contemporary consumer products, from sports socks to washing machines.”

14. Ibid.

15. “Constantly Battling a Hidden Foe,” New York Times, October 8, 2017, p. SP1.

16. See World Silver Supply and Demand at https://www.silverinstitute.org/site/supply-demand/.

17. “Teheran Students Seize U.S. Embassy and Hold Hostages,” New York Times, November 5, 1979, p. A1.

18. The price of spot silver (i.e., for the November contract on the Commodity Exchange) closed at $16.08 on November 2, 1979 (the last trading day before the hostage taking) and reached a high of $50.36 on the Commodity Exchange on January 18, 1980 (see note 2).

19. One measure of the relative size of the gold and silver markets comes from futures markets. Data for the Commodity Exchange on December 31, 2014, show a total open interest (total number of contracts outstanding) for gold of 371,646 contracts and a total of 151,215 contracts for silver. These translate into dollar amounts as follows: Gold contracts are for 100 ounces and the cash price per ounce on December 31, 2014, was $1,184, for a total of $44 billion. Silver contracts are for 5,000 ounces at a cash price of $15.69 per ounce for a total value of $11.9 billion. These numbers are surely underestimates of the total value of gold and silver in the world, but the relative size of the two markets is confirmed by a completely different source and time period. U.S. Department of Commerce, The Minerals Yearbook: 1932–1933 Year 1931–32 (Washington, DC: Government Printing Office, 1933), p. 12, estimates the total value (at the much lower prevailing market prices) of all gold mined since 1493 as $22.9 billion versus $14.6 billion for the total value of silver.

20. Using the same three-year time period as in the earlier note for silver, the cash price for gold on September 12, 2008 was $766 per ounce and on September 12, 2011 it was $1,814 per ounce, for an increase of 237%.

21. See Milton Friedman, Money Mischief: Episodes in Monetary History (New York: Harcourt Brace & Company, 1994), pp. 249–60.

22. David Ricardo, The Principles of Political Economy and Taxation (London: John Murray, 1817), pp. 506–7.

23. I have added silver in brackets in the quote based on a footnote in ibid., p. 503: “Whatever I say of gold coin is equally applicable to silver coin; but it is not necessary to mention both on every occasion.”

24. Among the most useful of the numerous studies of this incident are: Francis A. Walker, “The Free Coinage of Silver,” Journal of Political Economy 1, no. 2 (1893); Walter K. Nugent, Money and American Society; 1865–1889 (New York: Free Press, 1968), esp. chap. 12–13; Friedman, Money Mischief, chap. 3.

25. The highest price during this twenty five year period was $1.29375 in 1874 and the lowest price was $.5275 in 1897. See U.S. Mint, Annual Report of the Director of the Mint for the Fiscal Year Ended June 30, 1936 (Washington, DC: Government Printing Office, 1936), p. 88.

26. See, for example, the reference in a speech by Representative Charles H. Grosvenor of Ohio on February 3, 1896, 54th Cong., 1st sess., Congressional Record and Appendix, 27, pt. 7, App. p. 83.

27. I collected daily quotes published by Handy & Harman from the Wall Street Journal during the 1930s, and the data show a low of 24.25¢ per ounce on December 29, 1932. According to Herbert M. Bratter, Silver Market Dictionary (New York: Commodity Exchange, 1933), p. 99, “The New York ‘official’ price is determined and issued daily, usually in the late forenoon, by Handy & Harman, and is based upon the market prices prevailing that day up to the time of such determination for nearby delivery in New York of spot silver in round amounts of 50,000 ounces.”

28. For a contemporary discussion, see James D. Paris, Monetary Policies in the United States: 1932–1938 (New York: Columbia University Press, 1938), pp. 48–49.

29. Ibid., p. 42.

30. “Pittman, Silver Pact Author, Sees Export Trade Increase,” Washington Post, December 22, 1933, p. 8

31. For a description of Chinese silver exports see “Shanghai Silver Again Moves Out,” New York Times, September 12, 1934, p. 13 and “Lower Silver Price Seen Necessary to End Smuggling,” Wall Street Journal, p. 1. On abandoning silver, Milton Friedman argues, “If the United States had not driven up the U.S. dollar price of silver, China would have left the silver standard later—perhaps several years later—than it actually did and under better economic and political conditions,” in Friedman Money Mischief, pp. 177–78.

32. See John Morton Blum, From the Morgenthau Diaries , vol. 1, Years of Crisis, 1928–1938 (Boston: Houghton Mifflin Company, 1959), p. 204.

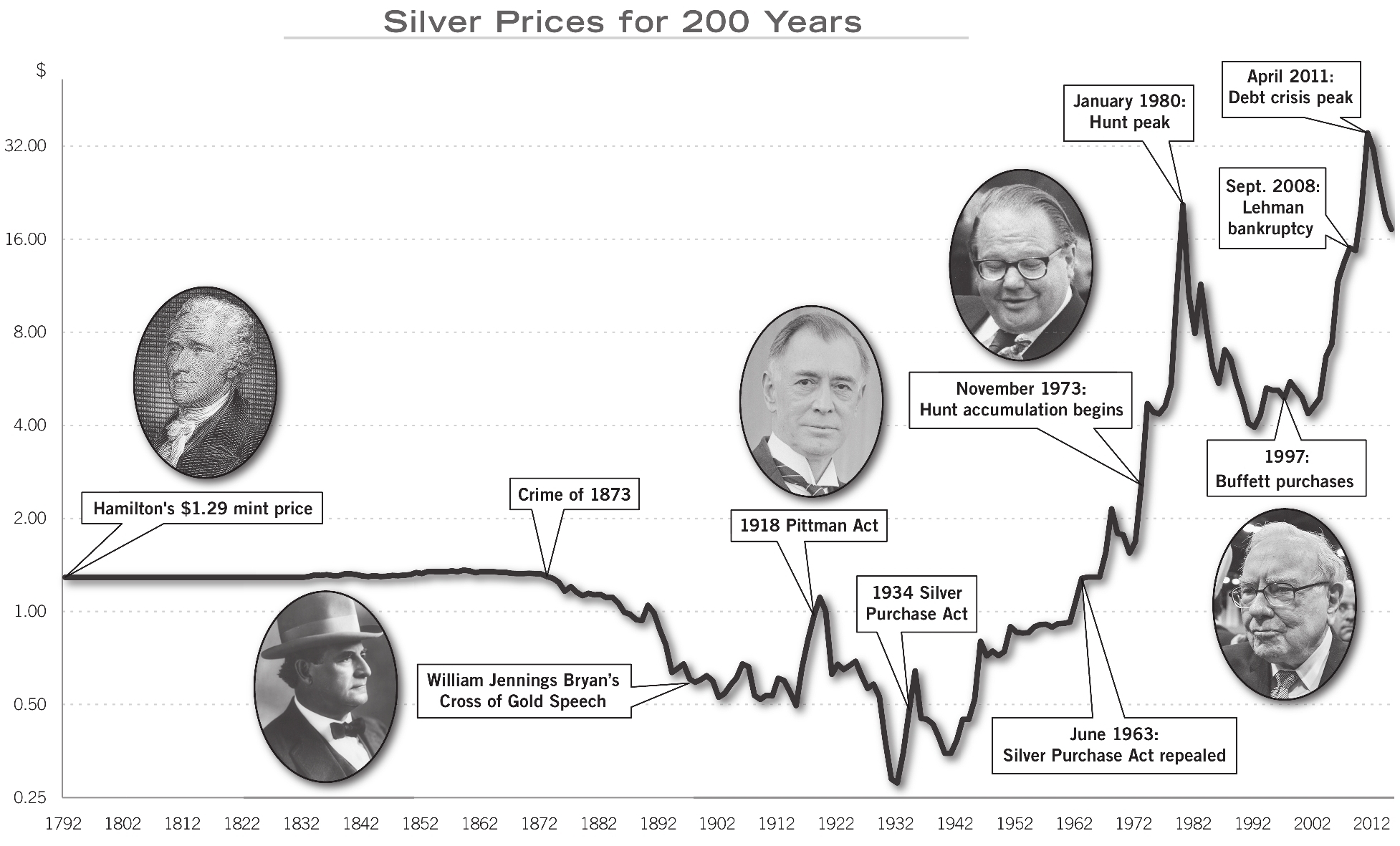

This semi-log chart shows the annual average price per troy ounce of pure silver in U.S. dollars from 1792 through 2015 and some of the major events influencing the white metal during that period. The data are spliced from the following sources: 1) The U.S. Mint price from 1792–1833; 2) The average market price reported by the Department of the Mint, 1834–1909; 3) The average of monthly prices reported by the CRB database, 1910–1946; 4) The average of daily prices reported by the CRB database, 1947–2015. The annual average price in 1980 is lower than in 2011, even though the daily peak price ($50) was higher in 1980, because daily prices fell more precipitously during 1980 compared with 2011. Note: Because of inflation, the value of $1.29 in 1792 is equivalent to $31.30 in current dollars of 2011, when silver hit a peak of $48 (based on the consumer price index calculator from the EH.net website of the Economic History Association).

|

Copyright © 2019 by Princeton University Press

Published by Princeton University Press

41 William Street, Princeton, New Jersey 08540

6 Oxford Street, Woodstock, Oxfordshire OX20 1TR

press.princeton.edu

All Rights Reserved

LCCN 2018941299

ISBN 9780691175386

British Library Cataloging-in-Publication Data is available

Editorial: Peter Dougherty and Jessica Yao

Production Editorial: Natalie Baan

Text and Jacket Design: Leslie Flis

Production: Jacqueline Poirier

Publicity: James Schneider

Jacket Credit: 1879 US silver dollar

This book has been composed in Sabon LT Std Roman

Printed on acid-free paper. ∞

Printed in the United States of America

1 3 5 7 9 10 8 6 4 2

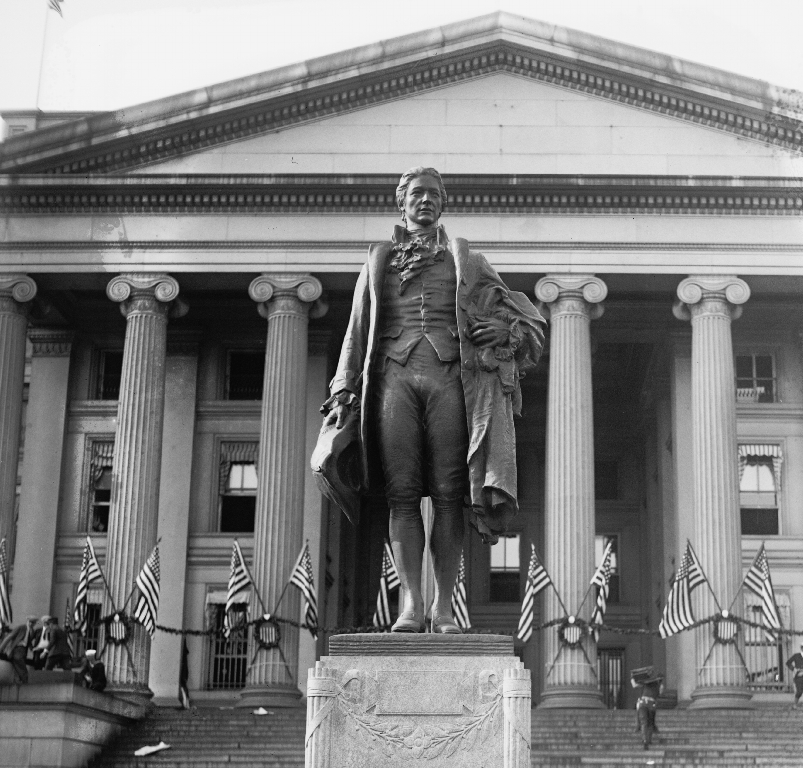

Figure 1. Hamilton graces the Treasury.

|

Alexander Hamilton knew more about money and finance than just about anyone at the Constitutional Convention. He was born out of wedlock in the West Indies around 1755, came to New York City in 1773, where he studied at King’s College, now Columbia University, and became an American patriot. He joined the New York militia to fight the British during the Revolution and served on George Washington’s Continental Army staff for most of the War. Following the victory, he helped found the Bank of New York, which survives today as Bank of New York Mellon, but soon turned his attention to remedying the loose connection among the states under the Articles of Confederation. He championed the establishment of a strong central government in the Federalist Papers, authored with James Madison and John Jay, and during the Constitutional Convention proposed a lifetime term for the American president like Britain’s King George III. Washington disagreed with Hamilton’s royalist instincts, of course, but put his young protégé’s financial skills to work by appointing him Treasury secretary in his first cabinet.1

Hamilton had more success implementing British traditions in his new job. He prepared a 1791 report “On the Establishment of a Mint” that recommended defining the U.S. dollar in terms of gold and silver, like the legal bimetallic standard prevailing in England.2 The resulting legislation of April 2, 1792, created a number of American coins, including a silver dollar weighing about three-quarters of an ounce and a ten-dollar gold eagle weighing about half an ounce.3 The precious metal content was specified precisely as 371.25 grains of pure silver for the dollar and 247.5 grains of pure gold for the ten-dollar eagle, and Hamilton recommended a version of Britain’s Trial of the Pyx to ensure accuracy.4

The British trial dates back to the thirteenth century and was designed to protect the King’s currency from being debased by the Master of the Mint producing coins with less precious metal content than the sterling standard. Coins were randomly selected from the mint’s production, locked in a chest (called the pyx) from one trial to the next, and were assayed by independent experts. A favorable verdict assured the public of its currency’s intrinsic value, while a negative outcome led to an indictment of the Master of the Royal Mint. Giles de Hertesbergh, who became Master of the Mint in 1316, was convicted of shortchanging the currency and spent six weeks in London’s Marshalsea Prison along with smugglers, debtors, and pirates.5

The 1792 act followed Hamilton’s proposals and required that an annual sample of coins be “assayed under the inspection of the Chief Justice of the United States, the Secretary and Comptroller of the Treasury, and the Attorney General of the United States,” a jury that rivals the best of Britain, but the punitive stage of the legislation took on a distinctly American flavor.6 Section 19 provided that if any of the coins were “debased or made worse … every such officer or person who shall commit any or either of the said offenses shall be deemed guilty of felony, and shall suffer death.”7

Capital punishment has always been serious business in the United States, with somber witnesses to executions on death row heading the list. Although no one was put to death in almost two hundred pyx trials (at least not publicly), the potential remained until President Jimmy Carter effectively ended the drama in 1977 by abolishing the U.S. Assay Commission, the agency charged with testing the coins.8 The Carter Administration called it a much-needed cost-cutting move, but voters failed to appreciate the president’s penny-pinching and, for other reasons too numerous to mention, rejected his reelection bid in 1980.

Most of Hamilton’s 1791 Mint Report focused on tying the U.S. dollar to gold and silver so that anyone with either metal could bring in bullion and receive coins in exchange, which is how currency was created back then. Hamilton considered gold by itself because of its stability and “greater rarity” but concluded that eliminating either metal from coinage would “abridge the quantity of circulating medium” and expose the country to the “evils of a scanty circulation.”9 A successful medium of exchange treads gently between scarcity and excess, like the ebb and flow of a mighty river, and nurtures commerce when the forces balance. Silver dominated as money in ancient times because it was valuable and remained the key circulating currency throughout Europe for hundreds of years because it never became too valuable.10 Hamilton promoted silver to avoid deflation and to sustain economic growth, and Congress made both precious metals legal tender in America, acceptable in the payment of debts and taxes. Gold’s greater value made it especially useful for large business transactions, like importing a case of French champagne, while silver was better for smaller social events, like buying a round at the local tavern.

Hamilton agonized over the relative gold and silver content of the dollar, knowing that incorrect ratios resulted in circulation of the overvalued coin while the undervalued would remain bullion. This well-known pitfall, called Gresham’s law after Sir Thomas Gresham, who helped Queen Elizabeth I reestablish the purity of the British pound, goes by the popular phrase “bad money drives good money out of circulation.”11 Sir Isaac Newton, the great scientist who had a second career as Britain’s Master of the Mint in the early eighteenth century, fell victim to Gresham’s law by inadvertently overvaluing gold and driving silver out of circulation.12 Many doubt that Gresham ever said the phrase, but history has been kind to Sir Thomas and his law just as it has been to Mr. Murphy and his law—If anything can go wrong, it will—whether or not he said it.

A simple example illustrates Gresham’s law. Suppose jewelers and silversmiths are willing to pay one dollar per ounce of gold or silver bullion and the mint follows suit and establishes a dollar coin containing an ounce of either metal. Owners of bullion would come to the mint to have the metal assayed for free and receive a dollar coin, so both metals would circulate as currency. Now suppose gold bullion rises in value to $2 per ounce because doctors say that eating gold flakes for breakfast makes you skinny.13 The mint continues to pay one dollar for either metal because that is the legal definition of each coin but now everyone hoards gold and brings only silver to be coined. Gold would no longer serve as currency because it is more valuable as a diet supplement.

Both coins circulate under a bimetallic standard, avoiding the “evils of a scanty circulation,” only when mint prices reflect market values. After much discussion Hamilton proposed a price ratio of fifteen-to-one at the mint because gold bullion was worth about fifteen times an equal weight of silver in 1791.14 The precious metal content of each coin in the 1792 Coinage Act resulted in a mint price of $1.29 per ounce of silver and a gold price fifteen times larger, $19.39 per ounce.15 These relative prices worked perfectly for about ten years, until the market value of gold relative to silver rose to almost 16 to 1, and citizens hoarded the yellow metal and brought only silver to the mint, just as Gresham predicted.16

1. Hamilton refuted the alleged “monarchial” tendencies, according to Rich ard Sylla, Alexander Hamilton (New York: Sterling Publishing Company, 2016), p. 102.

2. Alexander Hamilton, On the Establishment of a Mint, 1st Cong., 3d sess., January 28, 1791, American State Papers: Finance, 1st Cong., 3d sess., vol. 1:91-100, available at

https://memory.loc.gov/cgibin/ampage?collId=llsp&fileName=009/llsp 009.db&recNum=3 009.db&recNum=3

3. See Establishing a mint and regulating the coins of the United States, 2d Cong., 1st sess., April 2, 1792. Statutes at Large, 2d Cong., 1st sess., vol. 1:246-251, available at

https://memory.loc.gov/cgibin/ampage?collId=llsl&fileName=001/llsl001.db&recNum=2/llsl001.db&recNum=2.

Section 9 of the act sets forth the precise grains of gold and silver that appear in the next sentence of the text as well as the total weight of each coin when an alloy metal (not specified) is added. The total weight of the silver dollar is specified as 416 grains, and, since there are 480 grains in a troy ounce, the silver dollar weighed 416/480 or .866 troy ounces. It contained 371.25 grains of pure (.999 fine silver) so the silver dollar was .8924 (371.25/416) pure. This was changed by the act of January 18, 1837, to .90 pure by reducing the size of the coin to 412.5 grains. Section 9 specified the ten dollar gold eagle as containing 247.5 grains of pure gold and a total weight of 270 grains for a purity of .9166 (247.5/270) and weighing a total of .5625 troy ounces (270/480). This was later changed by a June 28, 1834 act, modified by the act of January 18, 1837, as follows: the pure gold content of the eagle was reduced to 232.2 grains with a total weight of 258, which made the eagle .9 pure gold and weighing .537 ounces (258/480). The updated details on silver appear in Dickson Leavens, Silver Money (Bloomington, Ind.: Principia Press, 1939), p. 20, and the updated details on gold are from H.R. Lindeman, Money and Legal Tender in the United States (New York: G.P. Putnam's Sons, 1879), pp. 24-27.

4. Hamilton's report of January 28, 1791, On the Establishment of a Mint, discusses the trial of the pix [sic] in the last paragraph.

5. John Cragg, The Mint (London: Cambridge University Press, 1953), p. 61.

6. The quotation is from section 18 of the act of April 2, 1792, Establishing a mint and regulating the coins of the United States.

7. Ibid., section 19.

8. See Thomas K. Delorey, “The Trial of the Pyx,” at

https://www.hjbltd.com/#!/article/235-the-trial-of-the-pyx/departments/articles/details.asp?inventorynumber=33&linenum=23

9. The full quote is “To annul the use of either of the metals as money, is to abridge the quantity of circulating medium, and is liable to all the objections which arise from a comparison of the benefits of a full, with the evils of a scanty circulation.” See Hamilton, “On the Establishment of a Mint,” p. 93.

10. The earliest coins discovered by archeologists were made of silver and date from the middle of the Iron Age, 800-900 BCE. See Raz Kletter and Etty Brand, “A New Look at the Iron Age Silver Hoard from Eshtemoa,” Zeitschrift des Deutschen Palästina-Vereins Bd. 114, H. 2 (1998): 139-154; and Christine M. Thompson, “Sealed Silver in Iron Age Cisjordan and the Invention' of Coinage,” Oxford Journal of Archaeology 22, no. 1 (2003): 67-107. This discovery negates the story of Greek historian Herodotus, who attributed the invention of coins to King Croesus of Lydia around 600 BCE. See Peter Bernstein, The Power of Gold: The History of an Obsession (New York: Wiley, 2000), pp. 27-37.

11. See Arthur J. Rolnick and Warren E. Weber, “Gresham’s Law or Gresham’s Fallacy,” Journal of Political Economy 94, no. 1 (1986): 17–24, for a more precise discussion.

12. Feavearyear, Pound Sterling, p. 155, cites Newton’s report, “Gold and Silver Coin,” Cobbett’s Parliamentary History (London, T.C. Hansard, 1811), 7:525–30, showing that he did not foresee the dominance of gold: “If things be let alone till silver money be a little scarcer the gold will fall of itself.”

13. Gold flakes made the New York Times on December 21, 2016, p. A25, with the headline “Police Identify Man They Say Took Gold Flakes from Truck.” The flakes, which are shed as jewelers work with gold, are collected and stored in buckets before being shipped by armored truck to a depository. The stolen bucket weighed eighty-six pounds and was valued at $1.6 million.

14. Hamilton, “On the Establishment of a Mint,” p. 94.

15. Section 9 of the act specifies the one dollar coin as containing 371.25 grains of pure silver and the ten dollar eagle as containing 247.5 grains of pure gold. These translate into prices as follows: An ounce contains 480 grains, so to get an ounce of pure silver you need 480/371.25 or $1.29293. The ten dollar eagle contains 247.5 grains, so to get 480 grains of gold (an ounce) you need 480/247.5 or $19.3939.

16. The increased relative value of gold during this period arose from expanded silver production in Mexican mines that entered the United States via trade. For details see J. Laurence Laughlin, The History of Bimetallism in the United States (New York: D. Appleton and Company, 1897), pp. 47–48. Also see Peter Temin, “The Economic Consequences of the Bank War,” Journal of Political Economy 76, no. 2 (1968), esp. pp. 267–70, for details on imports of silver from Mexico and exports to China.

|

Figure 2. A familiar Alexander Hamilton.

|

The emergence of a silver standard from the framework of bi-metallism probably displeased Hamilton, but not for long. He was killed in America’s most famous duel on July 11, 1804, by Aaron Burr, the sitting vice president of the United States. Bad blood had soured their relationship over many years. Hamilton supported Thomas Jefferson over Burr in the contested presidential election of 1800 and the former Treasury secretary supposedly denigrated the vice president, who ran for governor of New York in 1804. But the underlying tension probably began much earlier: Burr had studied at the College of New Jersey, now Princeton University, making the King’s College (now Columbia)-educated Hamilton a natural Ivy League rival.

Hamilton could not amend his handiwork but Congress did it for him in 1834 (with further adjustment in 1837) by redefining the gold content of the dollar and increasing the mint price per ounce to $20.67.17 The new mint price ratio of gold to silver of 16 to 1 ($20.67 divided by $1.29) overvalued gold compared with the bullion market and encouraged Americans to turn the yellow metal into coins, which they did.18 Going forward gold served as the primary medium of exchange in America even though both silver and gold were legal tender, acceptable in payment of debts and taxes. Silver was relatively more valuable as bullion than as coins at 16 to 1, with an average price in the metals market greater than the mint price of $1.29 per ounce in every year from 1834 through 1873.19 The highest annual average price per ounce of silver was $1.36 in 1859, when the discovery of the giant Comstock Lode was publicized, marking a peak in value for the white metal. The average yearly price of silver would fall well below that level for the next hundred years and make the 16 to 1 price ratio a distant memory.20

The Comstock Lode, centered in Virginia City, Nevada, a rocky outcropping in the middle of nowhere, produced more silver in its first ten years of operation than America had ever seen. Thousands of settlers from across the country, plus immigrants from countries such as Ireland, France, Germany, and China, swarmed into the barren wasteland to seek their fortune, transforming the slopes of Mount Davidson into the bustling metropolis of 30,000 called Virginia City.21 The steep grade of the mountainside made daily life an adventure, frequently forcing citizens to take cover when they heard the rumble of runaway wagons rolling down C Street in city center. But vigilance and perseverance paid dividends to those who survived the dust and dirt of frontier living. Mining companies such as Keystone, Ophir, Yellow Jacket, and Uncle Sam (of course) extracted about $30 million in silver from the Comstock Lode from 1861 through 1870 compared with less than $2 million produced in the entire United States from the founding of the Republic until then.22

This mining bonanza had a much broader impact on American life than simply turning a few pick axes into silver spoons. It launched the career of America’s most famous nineteenth-century humorist, Samuel Clemens, who took the name Mark Twain as a reporter for Virginia City’s Territorial Enterprise; it brought Nevada into the Civil War on the Union side as America’s thirty-sixth state on October 31, 1864; and a century later it spawned the NBC TV hit western Bonanza, which aired from 1959 through 1973 and whose title references the giant discovery in the region called the Big Bonanza.23 Some blame the Comstock Lode with triggering a collapse in silver prices that ultimately led to the 1896 presidential candidacy of William Jennings Bryan and the confrontation between East Coast bankers and midwestern farmers. The evidence shows that the Virginia City mines were a sideshow.

Despite the jump in silver production from the Comstock Lode during the 1860s the price of bullion remained remarkably constant, averaging between $1.35 per ounce in 1860 and $1.33 in 1869.24 The 50% price decline during the remainder of the nineteenth century began in 1873, when silver fell below $1.30 per ounce for the first time in almost thirty years, and continued to slide like those runaway wagons in Virginia City.25 The year 1873 was the date of an alleged crime, when Senator John Sherman, chairman of the Senate Finance Committee, guided the Coinage Act through Congress, eliminating the silver dollar as legal tender in the United States. Silver’s vulnerability began with the California gold rush a generation earlier, and Sherman fed the avalanche with deliberate deception.

17. Congress lowered the gold content of a dollar from 24.75 grains to 23.2 grains in 1834 and then made it 23.22 in 1837. Less gold in the dollar meant it cost more dollars to buy an ounce. Since there are 480 grains in a troy ounce, it took $20.67 (480/23.22) to buy an ounce of gold. See Leavens, Silver Money, p. 20.

18. Laughlin, History of Bimetallism, p. 61, says that there was a purposeful overvaluation of gold in 1834 to accommodate political pressure in Congress after gold was discovered in North Carolina and other southern states. Laughlin also suggests (p. 65) that Congress overvalued gold “inasmuch as the value of silver relatively [sic] to gold had been steadily falling for many years, [and Congress thought] it was quite likely to continue to fall still more in the future.” The 16 to 1 ratio was designed to anticipate a further deterioration in relative market prices, which did not occur, hence the overvaluation remained and drove silver out of circulation.

19. Data on average silver prices in each year between 1833 and 1935 (based on London quotations) are in the Annual Report of the Director of the Mint, p. 89. Two other sources are available with similar (within a penny) numbers over that time period. Page 88 of the Annual Report provides estimates of the New York price from 1874 through 1935. And the NBER Macrohistory Database at

http://www.nber.org/databases/macrohistory/contents/chapter04.html

also records London prices like those on page 89 of the Annual Report. Monthly data from the Commodity Research Bureau are available from 1910 through 1946 and then are available daily beginning January 1947.

20. The annual average price of silver was $1.578 per ounce (an average of monthly data on cash silver from the Commodity Research Bureau database) in 1967, the first time the annual average exceeded $1.36 since 1859. Two spikes in daily silver prices (New York quotations) in 1919 and 1920 exceeded $1.36 (see page 88 in the Annual Report) but the annual averages in those years were below $1.36. Roy Jastram, Silver: The Restless Metal (New York: John Wiley & Sons, 1981), p. 86, reports that silver “exploded to $1.375 in November 1919.” Bratter, Silver Market Dictionary, p. 113, writes: “The maximum price of silver recorded in New York was $1.38¼ on November 25, 1919.”

21. Ronald M. James, The Roar and the Silence: A History of Virginia City and the Comstock Lode (Las Vegas: University of Nevada Press, 1998), esp. p. 35.

22. See the discussion and table on page 1 of the “Special Report to the Monetary Commission on the Recent and Prospective Production of Silver in the United States, Particularly from The Comstock Lode,” in Report and Accompanying Documents of the United States Monetary Commission, organized under Joint Resolution of August 15, 1876, 2 vol., 44th Cong., 2d sess. S. Rept 703 (Washington, DC: Government Printing Office, 1877). The total production during this period for the entire United States was $100 million in silver. During 1861 the output was $2 million, all from Comstock, and in the last year output was $16 million, of which $5 million came from Comstock. I used 5/16 as my estimate for Comstock for the entire period, which is probably too low.

23. See James, Roar and Silence, pp. xix–xx.

24. These data on average silver prices are for the bullion market in London and come from the Annual Report of the Director of the Mint, p. 89.

25. The last year silver averaged less than $1.30 was in 1845, when it was $1.298.

|

Figure 3. A relaxed Senator John Sherman.

|

Republican John Sherman of Ohio spent almost half a century in Washington, D.C., as an influential legislator and cabinet member. He was elected to Congress in 1854 and then to the U.S. Senate in 1861, becoming a staunch supporter of Abraham Lincoln during the Civil War. He would later serve as secretary of the Treasury under Rutherford B. Hayes and as secretary of state under William McKinley but is most famous for sponsoring what became known as the Sherman Antitrust Act passed in 1890, the favorite legislation of trust-busting President Teddy Roosevelt. Few remember Sherman’s role as chairman of the Senate Finance Committee in the alleged Crime of 1873, which is exactly what he wanted.

Sherman was born in Lancaster, Ohio, in 1823, one of eleven children, to Charles and Mary Sherman.1 His father was a successful lawyer who died when John was six years old but still served as an example. John became a lawyer like his father and then used his legal training, like many before and since, to launch a political career. He accumulated considerable legislative power during his tenure in Washington and twice pursued, but failed to become, the Republican presidential candidate. Throughout his career, he suffered in the shadow of an older brother, Civil War General William Tecumseh Sherman, who replaced Ulysses S. Grant as Commanding General of the Army after Grant became president. General Sherman had gained fame for his brutal “march to the sea” through Georgia during the war but soon became an engaging and entertaining public speaker. He turned down subsequent requests to become a presidential candidate by famously saying, “I will not accept if nominated and will not serve if elected.”2 Sibling rivalry aside, Senator Sherman, known as the “Ohio icicle” for his austere personality, would have denied allegations of deception in the Coinage Act of 1873, but public admiration for his gregarious brother, called “Cump” by family and friends, must have encouraged the cover-up.3

The Crime of 1873 refers to legislation passed by Congress on February 12, 1873, negating Alexander Hamilton’s favorite law, that both gold and silver be monetary standards in the United States, and establishing gold as sole legal tender for all obligations.4 The new law omitted the free and unlimited coinage of silver dollars at the mint, an option since 1792, and restricted the legal tender status of subsidiary silver coins, like dimes, quarters, and half-dollars, to five dollars or less.5 The U.S. Constitution allows Congress to “coin money” and “regulate the value thereof,” so no legislator voting for the act committed a crime in the technical sense. Senators and congressmen could even make their favorite coins of Great Britain, France, Spain, and Portugal legal tender in the U.S., which they did in 1793, without violating the law.6 The allegations of impropriety arose because few people realized the full consequences of the shift to gold when the law was passed. Moreover, Senate Finance Committee Chairman John Sherman, who introduced the legislation, not only failed to sound the warning bell but also soft-pedaled the bill despite knowing its importance.

Sherman said on the Senate floor during an early discussion of the Coinage Act,7 “This is a bill to codify the mintage laws of the United States. It does not adopt any new principles; it makes but very few changes in the general laws, except to transferring the head of the Minting Bureau to Washington.”8 Sherman should have stopped after the first sentence, which accurately described the legislation. More than fifty of the sixty-seven sections of the Coinage Act of 1873 deal with the minting process, including the salaries and responsibilities of the assayer, melter, refiner, and coiner, as well as administrative matters, such as making the mint a bureau within the Treasury Department rather than a free standing agency.9 Much of the associated debate in Congress focused on whether the mint should charge a fee for coining bullion.10 These housekeeping details on minting pushed the legislation’s substantive change in the monetary standard beneath the radar of even sophisticated observers, like Francis A. Walker, a professor of political economy who had been lecturing on the topic of money at Yale in 1873. An avid newspaper reader with close friends in New York business circles, Walker confesses not to have “learned of the demonetization of the silver dollar” until long after it had happened.11

The word “crime” to describe the 1873 Act was first used by George M. Weston, secretary of the U.S. Monetary Commission of 1876, who wrote, “It is impossible to doubt that the laws of the country have been tampered with. Who the perpetrators of this crime were is not likely ever to be satisfactorily known.”12 Senator John P. Jones of Nevada called it a “grave wrong” to remove silver as a monetary standard “under the guise of regulating the mints of the United States.”13 Others called it a “fraud” and “conspiracy,” but Professor Walker, who would become president of MIT as well as the founding president of the American Economic Association, set the proper tone of condemnation: “No man in a position of trust has a right to allow a measure of such importance to pass without calling attention sharply to it, and making sure that its bearings were fully comprehended. And no man who did not know that the demonetization of silver by the United States was a measure of transcendent importance, had any right to be on such a committee or to put his hand to a bill which touched the coinage of a great country.”14

1. For background see chapters 1 and 2 in John Sherman’s Recollections of Forty Years in the House, Senate, and Cabinet (Chicago: Werner Company, Chicago, 1895), available at

https://archive.org/details/johnshermansreco00sher

2. See William Kolasky, “Senator John Sherman and the Origin of Antitrust,” Antitrust 24, no.1 (2009): 85.

3. Ibid., for the nicknames. In American Statesman: John Sherman (Boston: Houghton Mifflin Company, 1906), p. 384, Theodore Burton writes about the senator’s personality: “The General was fond of meeting friends and loved society. … The Senator … was much more at home in the intellectual laboratory in which his work was performed.”

4. See section 14 of the Coinage Act of 1873, more formally titled, “An Act revising and amending the Laws relative to the Mints, Assay offices, and Coinage of the United States,” 42d Cong., 3rd sess., February 12, 1873. Statutes at Large, vol. 17, chap. 131.

5. Section 15 of the Coinage Act of 1873 omits the silver dollar from the list of silver coins to be minted, and section 17 states: “That no coins, either of gold, silver, or minor coinage, shall hereafter be issued from the mint other than those of the denominations, standards, and weights herein set forth.”

6. “An Act Regulating Foreign Coins, and for Other Purposes” (February 9, 1793), Statutes at Large, 1:300–301.

7. This discussion relates to an earlier version of the bill, S. 859, introduced by Sherman in April 1870 and revised in December 1870, which also established gold as sole legal tender and made subsidiary silver coins legal tender only for payments up to one dollar (see sections 14, 15, and 18).

8. The Congressional Globe, January 9, 1871, p. 374.

9. These details are memorialized in the formal title of the legislation, “An Act revising and amending the Laws relative to the Mint, Assay Offices, and Coinage of the United States,” 42d, sess. 3 (February 12, 1873).

10. See Robert R. Van Ryzin, Crime of 1873: The Comstock Connection, (Iola, Wisc.: Krause Publications, 2001), chap. 10.

11. Walker, “Free Coinage of Silver,” p. 17n1.

12. See Paul M. O’Leary, “The Scene of the Crime of 1873 Revisited: A Note,” Journal of Political Economy 68, no. 4 (1960): p. 390, for the reference to Weston. The quote is from Report and Accompanying Documents of the United States Monetary Commission, 1, p. 193.

13. Paul Barnett, “The Crime of 1873 Re Examined,” Agricultural History 38 (July 1964): p. 178.

14. Walker, “Free Coinage of Silver,” p. 170.

John Sherman had become chairman of the Senate Finance Committee in March 1867 and knew almost immediately that silver’s role as a monetary standard would disappear like the recently extinct dodo bird.15 He toured Europe during the spring of 1867 and spent considerable time in Paris attending both the Universal Exposition, a world’s fair organized at the suggestion of French Emperor Napoleon III, and the international monetary conference, where representatives of twenty countries gathered to promote uniformity across borders in weights, measures, and coins.16 Sherman was treated like visiting royalty, referred to as “Monsieur le Senateur” while joining a reception given by the Emperor at the richly decorated Tuileries Palace adjacent to the Louvre.17 He donned evening attire, including dress coat, formal trousers, and black silk stockings, and was presented to the Empress of Russia, the Prince of Wales, the King of Prussia, and Bismarck, who Sherman proudly recalls, “recognized me with a bow and a few words.”18 But state formalities took a backseat to the international monetary conference for the future of silver in world commerce.

Amidst the distractions of Parisian nightlife, the conference focused on narrow questions like the universal adoption of the metric system and broader issues like the appropriate international monetary standard. Spurred by massive discoveries of gold in California and Australia in the 1850s, which cheapened the yellow metal and led to its dominance as the circulating medium (courtesy of Gresham), conference participants recognized that gold had become sufficiently plentiful to support growing world trade and no longer suffered from excessive scarcity compared with silver. Moreover, they cited the easy portability of gold relative to the white metal as an advantage for “international coins,” providing an ideal medium of exchange to settle trade among countries.19 The conference voted by “a great majority” that gold be “the sole monetary standard of value” and recommended abandoning “the system of double monetary standard [bimetallism] … wherever it exists.”20

Within six years of the Paris Monetary Conference nearly every major European country had moved towards the gold standard, and John Sherman wasted little time implementing its recommendations in the United States. He submitted a bill to Congress in 1868, based on the report of Samuel Ruggles, America’s representative to the international conference, called “In relation to the coinage of gold and silver.”21 The legislation headlined demonetizing silver and promoted a new five-dollar gold coin that would be interchangeable with a French coin of twenty-five francs. Section 3 of the bill emphasizes “that the gold coins to be issued under this act shall be a legal tender in all payments to any amount; and the silver coins shall be a legal tender to an amount not exceeding ten dollars in any one payment.” Opponents of the bill, led by Senator Edwin Morgan of New York, a former chairman of the Republican National Committee, ambushed the initiative by observing, “A change in our national coinage so grave as that proposed by the bill should be made only after the most mature deliberation.”22

Sherman learned from this battlefield setback and countered with a diversion strategy worthy of study at West Point. He introduced new legislation prepared by the Treasury in April 1870, called “Revising the laws relative to the mints, assay offices, and coinage of the United States.”23 The bill quietly buried the demonetization of silver under mind-numbing instructions to the mint, such as “the assayer shall assay all metals and bullion whenever such assays are required in the operations of the mint.”24 The proposed legislation also removed the link to the French franc. Most newspapers ignored the 1870 bill, as well as the resulting Coinage Act of 1873, and those publications that commented put the withdrawal of the silver dollar at the bottom of the pyramid.25

No one cared about the mint, other than residents of Philadelphia (where the main branch was located), and fewer worried about the silver dollar in 1873, which was an “unknown coin” in the country according to Sherman.26 And the senator was right.27 For more than a generation silversmiths had turned the white metal into forks and knives rather than letting it circulate as currency. The value of shiny cutlery at the dinner table was worth more per ounce than the mint price of $1.29. Sherman added a personal observation in his memoirs: “Although I was quite active in business which brought under my eye different forms of money, I do not remember at that time ever to have seen a silver dollar.”28

From Sherman’s perspective the legislation simply ratified the status quo, suggesting that no one would miss the silver dollar, and justifying his early observation that the bill “does not adopt any new principles.” But that perspective ignores an important aspect of bimetallism even when one metal dominates, as gold did in the decades before the Coinage Act of 1873. Alexander Hamilton made both gold and silver legal tender primarily to avoid the scarcity of circulating currency, to serve as a buffer against deflation, but that also gave taxpayers and debtors the option to pay their obligations in the cheaper metal. Everyone likes options, which, by definition, confer the right but not the obligation to do something, and are valuable even if they remain unused.

For example, homeowners value the right to refinance their mortgages, such as replacing a 6% loan with one costing 4% as interest rates decline, and that right facilitates the initial decision to borrow and buy a home. Few homeowners refinanced their mortgages in the United States during the 1970s because interest rates rose throughout the decade, and some may have forgotten how profitable refinancing could be, but no mortgage borrower would willingly abandon that option without a fight. Congressmen who quietly passed legislation to remove the refinancing option because it had fallen into disuse would have to find alternative employment after the next election.

During the decades before the Coinage Act of 1873 few Americans exercised the option to pay obligations in silver because the white metal was more valuable as bullion. In the colorful horseracing language of finance professionals, it was an out-of-the-money option because it failed to pay off, like the losing thoroughbreds in the Kentucky Derby, and that explains the giant yawn greeting the Coinage Act of 1873. But the market price of silver declined sharply soon after, making those out-of-the-money options quite valuable. The price of $1.29 per ounce at the mint looked cheap in 1872, when silver bullion averaged $1.32, but when silver hit $1.16 in 1876 that same mint price would have been a bonanza.

The Coinage Act was passed with the help of Sherman’s subterfuge, but that legislation did not precipitate the price slide that led to the outcry of criminal behavior. The price of silver had already reached the lowest point in more than twenty years in the London bullion market in December 1872, two months before the act became law.29 European countries dominated the demonetization of silver and the switch to gold, beginning with the Imperial Coinage Law in Germany, passed on December 4, 1871, at the urging of Chancellor Bismarck, and followed by Sweden and Denmark adopting gold in 1873.30 Belgium, Italy, France, and Switzerland moved towards the gold standard by restricting the free coinage of silver.31 France cut the maximum silver coinage to 250,000 francs per day in September 1873 and reduced it further to 150,000 francs in November.32 Holland ended the practice of buying silver at a fixed price in 1872 and stopped all silver coinage in 1873.33 In what appears like a coordinated ambush, massive sales of silver by Germany, which had been on a silver standard until then, combined with the absence of buyers from the rest of Europe, pushed down the price of the white metal to then unprecedented levels.34

The unlikely provocation for this European offensive against silver began in the gold mines of California, Russia, and Australia in the 1850s. Silver dominated gold as the preferred currency for most of recorded history primarily because it was scarce but not too scarce, so that it held its value but was sufficiently abundant to support expanding trade. But the explosion in gold production beginning in 1848 at Sutter’s Mill, California, coupled with discoveries in Russia and Australia, appeared to solve the gold shortage.35 Total world production in the twenty-five years between 1850 and 1875 matched the entire gold output of the previous 350 years.36 The growing circulation of gold coins and the natural advantage of gold as international money, settling large transactions in world trade because it is compact and inexpensive to ship, convinced representatives in 1867 at the international monetary conference to recommend the gold standard.37 And four years later, after Germany defeated France in the Franco-Prussian War, Bismarck rushed to adopt the conference recommendations. The Iron Chancellor wanted to create a German Goliath and what better initiative than to emulate Britain, the dominant economic superpower, which had been on the gold standard since 1816.38 The other European countries followed like anxious freshmen pledging for a fraternity.

15. He became chairman on March 4, 1867, when the fortieth Congress was sworn in. See Sherman, Recollections, p. 334. The flightless dodo became extinct during the seventeenth century.

16. Ibid., pp. 339, 420.

17. Ibid., pp. 342–43, describes this incident.

18. Ibid., p. 343.

19. See Report of the International Conference on Weights, Measures, and Coins, held in Paris, June 1867; and Report of the International Monetary Conference, held in Paris, June 1867 (London: Harrison and Sons, 1868), available at positions 5 and 6 (p. 51) discuss the advantages of gold as international money.

20. See Report of the International Monetary Conference. Page 52 discusses the consequence of gold discoveries: “Before the discovery of the rich mines of California, Australia, the North-west of the United States, and the American possessions of Great Britain, gold coins having a price greater than the legal rate were the first to go out of circulation, and could only be procured at a premium. After these discoveries the contrary was the case; gold having become lower than the legal rate, silver disappeared.” See page 55 for the discussion of Proposition 7 (against the double standard), which was put to a vote and “adopted by a great majority.”